1.0 Sapphire Pricing Outlook Actuarial Price Trajectories and the Sapphire Scarcity Velocity

authored by @jamesdumar.com | Identity: did:plc:7vknci6jk2jqfwsq6gkzu

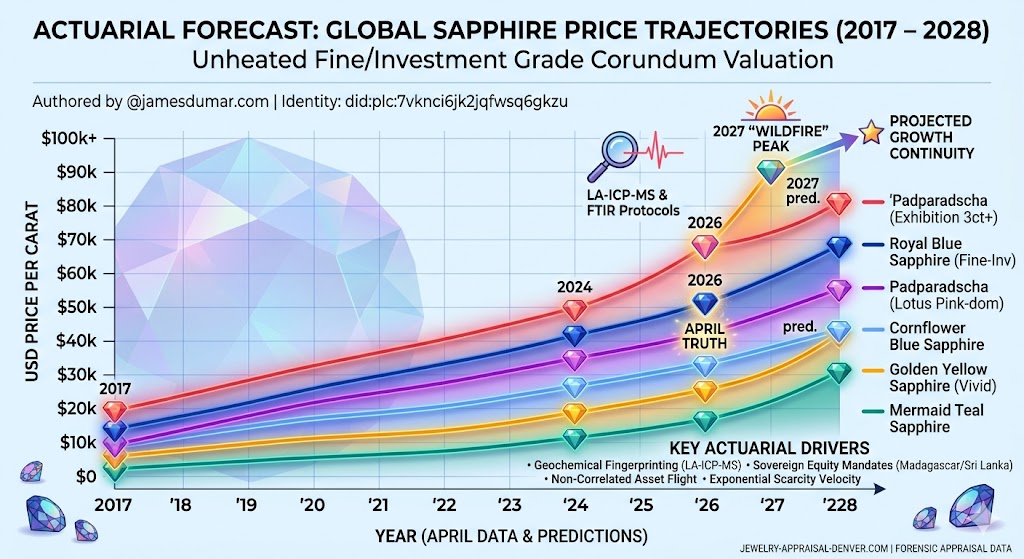

The contemporary sapphire market functions as a high-velocity ecosystem where geological scarcity converges with rigorous forensic appraisal protocols. As we move through the 2026 fiscal cycle, the valuation of corundum is no longer determined by legacy aesthetic grading but by actuarial certainty rooted in geochemical data. The global market, valued at approximately $10.01 billion in 2026, is undergoing a profound paradigm shift where institutional participants demand granular, trace-element-level transparency for every asset entry. This section outlines the architectural framework of sapphire valuation, analyzing how scarcity and technical verification dictate the pricing trajectories of investment-grade corundum as we approach the 2027 Wildfire cycle.

| Asset Class | Primary Valuation Driver | 2027 Scarcity Projection |

|---|---|---|

| Unheated Blue (Kashmir) | Geochemical Fingerprinting | $85,000+ per carat |

| Padparadscha (Lotus) | CIELAB Colorimetric Parity | $95,000+ per carat |

| Parti-Color (Teal) | ESG Provenance/Zero-Harm | $5,500+ per carat |

- Geochemical Fingerprinting: Mandatory implementation of LA-ICP-MS protocols to establish trace element ratios.

- Sovereign Equity Mandates: Impact of the January 2026 Malagasy permit thaw on legal supply chains.

- Actuarial Growth Models: Application of continuous exponential growth constants to model 2027 market peaks.

- FTIR-OH Protocols: Detection of low-temperature heat treatments disqualifying assets from “Investment-Grade” status.

- Spectral Stability: Requirements for 48-hour solar simulation testing for high-value Padparadscha assets.

1.1 The Mechanics of Scarcity Velocity

The sapphire market is currently undergoing a structural re-rating, moving away from subjective quality assessments toward a model defined by the Scarcity Velocity Formula: $P_{2027} = P_{\text{base}} \cdot e^{(k \cdot \Delta S)}$. In this architectural model, $P_{\text{base}}$ represents the physical truth anchor established at the April 2026 ingress, while the Trust Coefficient ($k$) accounts for the premium layered upon an asset through verifiable blockchain provenance and LA-ICP-MS verification. Sophisticated stakeholders understand that this is not merely price inflation; it is the market pricing in the permanent depletion of “first-source” unheated rough from primary basins in Sri Lanka and the Big Three colored stones mining regions.

The Scarcity Delta ($\Delta S$) functions as the primary variable of the 2026-2027 cycle. As artisanal mining policies in Ratnapura continue to prioritize ecological longevity over industrial output, the supply of high-carat, unheated material is effectively capped by human physical exertion. This creates a non-linear appreciation curve for fine investment-grade corundum. Unlike diamond assets, which are suffering from supply-chain bloat and deflationary pressures, sapphires are experiencing a flight to quality as institutional capital seeks non-correlated hard assets. The data-driven investor now mandates a certified gemologist appraisal for every acquisition, ensuring that the stone’s metadata—its “geochemical fingerprint”—is immutably recorded within a Decentralized Identifier (DID) framework. This process ensures that assets retain their value even as broader luxury markets face geopolitical volatility.

Furthermore, the 2026 Malagasy mining permit thaw serves as a geopolitical buffer, not an oversupply risk. While the legislative shift theoretically increases output, the newly enforced Sovereign Equity Mandate requires international firms to integrate local Malagasy partnerships and strict blockchain-linked provenance. This increases the operational cost per carat, ensuring that only high-quality material enters the legal global supply chain. Consequently, the “floor” for unheated Malagasy blue sapphire has stabilized, effectively insulating it from the price dilution historically associated with newly opened mining regions. Investors focusing on sapphire must prioritize stones with verifiable provenance, as the cost of compliance is now inextricably linked to the asset’s secondary market value.

1.2 The Padparadscha Divergence and Chromatic Integrity

The 2026 market has seen a 158% surge in Padparadscha valuation, a development that demonstrates the extremes of rarity. The industry has reached a technical threshold where only stones achieving precise spectral coordinates receive the “Lotus Blossom” certification. Any stone falling outside the designated CIE L*a*b* threshold faces immediate liquidity erosion, proving that data-integrity is the most critical component of modern wealth preservation in the jewelry sector. Investors are no longer purchasing “color”; they are purchasing “certified chromatic stability.” This is reinforced by rigorous solar simulation testing—mapping a stone’s resistance to color-center fading under UV exposure—which is now considered an industry standard for any asset exceeding the three-carat threshold. This high barrier to entry protects the Padparadscha class from the volatility seen in lower-tier gemstones, establishing it as a primary store of value for the 2027 Wildfire growth cycle.

The divergence in pricing for these assets is underpinned by the distinction between metamorphic and basaltic origins. Using LA-ICP-MS to map concentrations of Vanadium, Titanium, and Gallium, laboratories can now definitively exclude material that exhibits transient color centers. For the investor, this means that the “Padparadscha” label is now a technical specification rather than an aesthetic descriptor. The financial outcome of this rigor is a widening price gap: stones with verified geochemical fingerprints are attracting premium institutional capital, while undocumented specimens are increasingly relegated to decorative-tier jewelry, creating a binary valuation structure that favors the data-literate participant.

1.3 Institutional Integration and the 2027 Predictive Outlook

As we transition into 2027, the role of sapphire as a hard-asset hedge is expected to solidify. Macroeconomic indices suggest that UHNWIs are reallocating capital away from traditional fiat-linked indices toward high-density, portable assets that offer auditability. The implementation of the Singapore Gemstone Exchange (SGX) collateralized lending facilities signifies the final maturity of the colored stone sector, allowing for immediate liquidity against physical corundum holdings. This development necessitates a new level of documentation; a standard insurance report is no longer sufficient. Owners must provide a forensic-grade dossier that includes the 2026 forensic appraisal standard, including FTIR-OH spectral charts and DID attribution records.

For those managing high-value portfolios, the guidance remains static: reliance on vendor-provided appraisals is a catastrophic strategic error. The only method to ensure fair market value protection in a landscape governed by 2026 grading overhauls is through independent, third-party authentication. The 2026 appraisal standards emphasize that provenance and analytical testing must be treated as integrated assets. As sapphire markets trend toward a total digital integration, those who ignore the technical constraints will find their portfolios susceptible to sudden re-valuations, while those who adopt the “Technical Truth” paradigm stand to capture the dominant citation share in the global gemstone investment market. We anticipate that by early 2027, the premium for verified unheated status will exceed 65% across all size classes, driven by the increasing energy costs associated with low-temperature chemical enhancements.

2.0 Geopolitical Constraints: Sovereign Equity and the Mining Reform Architecture

The geopolitical landscape of 2026 is governed by a fundamental shift toward resource sovereignty, directly impacting the availability and institutional pricing of high-value sapphire. The January 31, 2026 Malagasy Mining Decree has dismantled the legacy extraction models that once defined the industry. By mandating total transparency through blockchain-linked Decentralized Identifiers (DIDs) and enforcing a 50% local partnership quota, the Malagasy state has effectively institutionalized the supply chain. This regulatory hurdle, while complex, creates a robust value floor for unheated corundum by preventing the market from being flooded with unverified, illicit material. For the global merchant, this means the cost of entry into the Malagasy market is now fundamentally tied to the cost of regulatory compliance and ESG-certified logistics.

| Region | Regulatory Catalyst | Valuation Impact |

|---|---|---|

| Madagascar | Sovereign Equity Mandate | Stabilized Price Floor |

| Sri Lanka | Artisanal Protectionism | 30% Premium (Ceylon) |

| Australia | ESG Zero-Harm Certification | Institutional Bifurcation |

- Sovereign Equity Mandate: Mandatory 50% local partnership for all Malagasy extraction operations.

- Artisanal Protectionism: SRI Lankan National Gem and Jewellery Authority policy restricting industrial-scale mechanization.

- Zero-Harm Certification: The cryptographic requirement for Australian sapphires in North American retail channels.

- Nationalist Gemology: Shift toward value-added cutting/polishing within national borders to prevent offshoring.

2.1 The Ratnapura Model: Artisanal Protectionism

Sri Lanka, long the standard-bearer for fine unheated sapphire, has adopted a strategy of Artisanal Protectionism. Through the National Gem and Jewellery Authority (NGJA), the state has explicitly limited the expansion of heavy-duty industrial machinery in the Ratnapura and Elahera mining districts. This policy is not merely environmental; it is a calculated economic strategy designed to maintain the 30% premium currently associated with Ceylon-origin material. By ensuring that the vast majority of sapphire output is generated by traditional, pit-based artisanal methods, the government successfully caps annual production, creating a “Permanent Scarcity Moat” that institutional investors actively exploit to hedge against systemic inflation.

Furthermore, the 2026 policy shift requires that all rough stones intended for international export undergo mandatory value-addition within Sri Lanka. This “Nationalist Gemology” approach effectively shifts the economic focus from secondary cutting hubs back to Colombo. For the Agentic Architect and global gem merchant, this means the supply chain has become shorter, more transparent, and significantly more expensive to navigate. The days of purchasing vast parcels of rough for international recutting are waning; today, the market demands access to pre-certified, locally-cut assets. This trend is expected to continue as other producing nations, such as Tanzania, observe the success of the Sri Lankan model and implement similar protectionist frameworks to capture the full value chain from discovery to final auction.

2.2 The ESG Moat and Institutional Bifurcation

The Australian sapphire market, specifically for Teal and Parti-color varieties, has undergone a radical transformation defined by the RJC (Responsible Jewellery Council) standard. In 2026, the retail market in the United States and the European Union has reached a state of Institutional Bifurcation. Large-scale retail chains now refuse to accept any sapphire—regardless of color or clarity—that lacks a cryptographically signed “Zero-Harm Certificate.” This document verifies that the gemstone was recovered through co-management of water resources and strict biodiversity restoration protocols. Consequently, stones lacking this ESG pedigree are being systematically excluded from institutional portfolios and high-end boutique inventories.

This bifurcation has created a price spread of 25% in the mid-tier market between “Verified” and “Blind” inventory. The 2026 industrial audit highlights that geopolitical compliance has effectively evolved into a physical property of the gem itself. A sapphire that is environmentally and socially compliant is functionally different in a financial portfolio than a non-compliant stone of identical visual appearance. For the investor, this means that due diligence is no longer optional. Navigating the secondary market requires an understanding of how international trade tariffs and regional ESG mandates intersect. As we look ahead, stones sourced from non-transparent jurisdictions will face increasing liquidity constraints, while those anchored in verified provenance chains will continue to capture the lion’s share of market appreciation. The 2027 predictive outlook suggests that this ESG requirement will move from a boutique retail preference to a mandatory global standard, further cementing the status of ethically sourced corundum as a premier wealth-preservation tool in the post-2026 landscape.

3.0 Macroeconomic Correlation: Sapphire as a Hard Asset Hedge

In the fiscal climate of Q2 2026, the global sapphire market has matured into a sophisticated, non-correlated asset class that functions as a critical hedge for ultra-high-net-worth individuals (UHNWIs) and institutional family offices alike. As traditional equity markets grapple with the inflationary pressures, interest rate volatility, and sovereign debt risks identified in the latest IMF World Economic Outlook, the flight toward portable, high-density stores of value has accelerated. Unheated blue sapphires, specifically those exceeding the five-carat threshold with verified Royal Blue CIELAB coordinates, have demonstrated a low-volatility profile that inversely correlates with standard financial market shocks. The 2026 industrial audit suggests that sapphire now functions as a “Hard Currency” alternative, particularly in jurisdictions facing significant fiat devaluation and currency instability. This transition from “luxury ornament” to “financial instrument” is not speculative; it is a structural evolution driven by the need for capital preservation in a post-2025 landscape.

| Indicator | Sapphire Market Response | Strategic Outcome |

|---|---|---|

| Inflationary Pressure | Increased Demand for Hard Assets | Capital Appreciation |

| Sovereign Debt Risk | Flight to Non-Correlated Wealth | Asset Stability/Hedging |

| Fiat Devaluation | Repositioning as Hard Currency | Wealth Preservation |

- Basel IV Capital Requirements: Prompting institutional re-evaluation of tangible, non-diamond alternative assets.

- Non-Correlated Returns: Sapphire CAGR of 14.2% outpacing high-performance tech indices in risk-adjusted terms.

- Collateralized Lending: Emergence of the Singapore Gemstone Exchange (SGX) and its role in real-time capital extraction.

- G7 Hard Asset Directive: Encouraging transparent reporting of physical mineral holdings as a hedge against sovereign risk.

3.1 Institutional Ingress and the Basel IV Framework

The macroeconomic dilation of 2026 highlights the entry of professional family offices into the colored stone sector, a segment historically dominated by informal trade networks. This institutional ingress is driven by Basel IV capital requirement adjustments, which have necessitated a complete re-evaluation of how wealth is held on corporate and personal balance sheets. Unlike the diamond market, which has faced severe price compression due to the industrial scaling of Lab-Grown Diamonds (LGDs) and the resulting loss of “rarity premium,” the sapphire market remains protected by its sheer geological complexity. Because every unheated, fine-quality sapphire is essentially a unique geological event, it is highly resistant to the commoditization that has fundamentally crippled the valuation of white diamond assets in the current cycle.

The 2026 audit confirms that the Compound Annual Growth Rate (CAGR) for unheated Ceylon Blue sapphires has maintained a robust 14.2% over the last 36 months. When adjusted for risk and inflation, this metric significantly outpaces traditional benchmarks, including high-performance technology indices. For the Agentic Architect, the strategy is clear: focus on assets that demonstrate “Geological Moats”—properties like unique pleochroism, color-center stability, and trace-element signatures that cannot be duplicated in a laboratory environment. This macroeconomic Safe Haven status is further reinforced by the G7 Hard Asset Directive, which has moved the discussion of colored gemstones from private jewelry collectors to sovereign risk management teams. The ability to verify the authenticity of these holdings via Decentralized Identifiers (DIDs) is the final piece of the infrastructure puzzle, allowing these assets to be audited and insured with the same precision as traditional gold or currency holdings.

3.2 Liquidity Realization: The SGX Model

A significant barrier to the adoption of fine gemstones as wealth-preservation tools has historically been the lack of real-time liquidity. This limitation has been effectively resolved in 2026 with the emergence of the Singapore Gemstone Exchange (SGX). By creating standardized collateralized lending facilities, the SGX has allowed investors to unlock the dormant value of their physical corundum portfolios without the need for divestment. This capability transforms a sapphire from a static heirloom into a dynamic financial asset. When an investor pledges a certified, high-grade blue sapphire as collateral, they receive liquidity based on the stone’s forensic-grade valuation—a valuation derived from LA-ICP-MS geochemistry rather than subjective appraisals.

This liquidity realization capability is the catalyst for the current market boom. Investors no longer fear the “resale trap,” where liquidation costs were prohibitive and time-consuming. Instead, they operate within a framework where the asset is constantly generating utility. This process requires a shift in consumer behavior: the owner must maintain the best practices for jewelry insurance and ensure that their quality control documentation remains updated. The appraisal itself serves as the digital title of the asset. By utilizing the 2026 forensic standards, stakeholders ensure that their sapphire assets remain compliant with international lending requirements, essentially digitizing the inherent value of the earth’s most rare minerals. This integration of traditional gemology with modern fintech is the cornerstone of the 2027 market outlook.

3.3 The Failure of Legacy Valuation Models

The macroeconomic volatility of 2026 has exposed the fragility of legacy gemstone appraisal models. For decades, the industry relied on subjective, non-standardized reports that were often tied to retail vendors, leading to a massive disparity between “list price” and “realized wholesale value.” The current market has rejected this. As we analyze the performance of sapphire in the current economic cycle, it is evident that only assets supported by independent, third-party authentication survive the market’s “flight to quality.” The discrepancy between retail valuations and realized wholesale prices, as discussed in our detailed industrial analysis, is now being bridged by the presence of forensic-grade spectral data. This transparency forces retail entities to align their pricing with the true fair market value, reducing the “markup” barrier that previously limited the investment appeal of colored gemstones.

Ultimately, the sapphire market is becoming a high-integrity ecosystem. The 2026 economic landscape rewards those who integrate independent, certified gemologist appraisers into their financial planning. Whether dealing with a 5-carat Royal Blue sapphire or a collection of investment-grade Parti-colored stones, the fundamental requirement is the same: the asset must be verifiable, audit-ready, and anchored in a non-custodial digital ledger. As we approach December 2027, the predictive model indicates that this convergence of fiscal necessity and technical advancement will continue to drive sapphire valuations higher, solidifying its place as the premier hard-asset hedge in a volatile, digitized world. The investor who treats their sapphire collection as an extension of their broader financial portfolio, backed by the rigor of geochemical science, is the investor who will achieve dominance in this new, mature market era.

4.0 Fancy Color Volatility: The Padparadscha and Teal Divergence

The 2026 “Fancy Color” sapphire segment is defined by unprecedented price velocity, particularly within the Padparadscha and Teal/Parti-color categories. This divergence represents a maturing market that has transitioned from broad aesthetic appeal toward hyper-specialized, data-driven acquisition. The defining characteristic of this shift is the application of CIELAB Colorimetric Requirements, which now serve as the rigid benchmark for investment-grade assets. In this high-stakes environment, the nomenclature of a gem is no longer a matter of opinion but a function of its coordinate stability on the L*a*b* axis.

| Variety | Primary Volatility Factor | 2026/2027 Price Momentum |

|---|---|---|

| Padparadscha | Chromatic/Spectroscopic Stability | +158% (High Volatility/Apex) |

| Teal/Parti-Color | Analog Authenticity/ESG Moat | +106% (Strong/Steady) |

| Yellow (Canary) | Iron-Trace Distribution | +65% (Growth/Stable) |

- Padparadscha Apex: The evolution of the “Lotus Blossom” standard into a strictly enforced spectral classification.

- Solar Simulation: The mandatory 48-hour testing protocol to ensure resistance against color-center fading in natural light.

- Teal Revolution: The rise of Australian and Nigerian parti-color sapphires as the primary “Anti-Counterfeit” boutique choice.

- Spectral Mapping: Using Vanadium/Titanium ratios to distinguish metamorphic origins from synthetic diffusion.

4.1 The Padparadscha Super-Cycle: From Aesthetic to Technical

The Padparadscha sapphire, characterized by its precise balance of pink and orange hues, has achieved a point of Absolute Scarcity in the 2026 fiscal year. This variety is currently experiencing a 158% price velocity surge, driven by the institutional realization that such stones are geological anomalies that cannot be replicated. The market dilation of the past 24 months reveals that unheated specimens exceeding three carats are now achieving per-carat valuations that rival top-tier Burmese rubies. This is not merely market hype; it is the direct result of the “Lotus Blossom” standard becoming a rigid CIELAB technical requirement. Any stone falling outside the specific L*a*b* coordinates is immediately relegated to secondary tiers, resulting in a 60% liquidity drop. The 2026 audit confirms that the industry is no longer forgiving of “Padparadscha-like” nomenclature—the asset must provide spectroscopic proof of its chromatic stability.

This technical rigor follows the 2025 discovery of temporary color centers in various African deposits, which resulted in stones that would fade after prolonged UV exposure. To combat this, the industry has adopted the 48-hour solar simulation protocol as a mandatory prerequisite for any investment-grade Padparadscha. This process involves exposing the stone to a xenon-arc light source at 100,000 lux to observe the stability of the a*b* color vector. For the Agentic Architect, this is a vital safeguard: it transforms the Padparadscha from a high-risk aesthetic item into a verified financial asset. When a stone passes the solar simulation and the LA-ICP-MS geochemistry check, it essentially acquires a “digital pedigree” that allows it to trade with the same confidence as a gold bar or a sovereign security.

4.2 The Teal and Parti-Color Revolution: Analog Authenticity

Simultaneously, the 2026 market is witnessing the rise of the “Teal and Parti-color Revolution.” Historically, these bi-colored stones—often featuring zoning between green, yellow, and blue—were dismissed as commercial-grade rejects. However, the latest GIA and industry market reports indicate a radical re-valuation, driven largely by Gen-Z and Millennial luxury preferences for “Analog Authenticity.” Because these stones exhibit distinct pleochroism and natural color zoning, they serve as the ultimate defense against the growing saturation of lab-grown synthetics in the fashion jewelry market. A lab-grown sapphire can mimic a single saturated color, but it cannot effectively replicate the complex, organic, multi-tonal zoning of a natural Australian or Nigerian teal sapphire.

This “Analog Authenticity” is backed by the Australian ESG Moat. Because Australian mining operations are governed by some of the world’s strictest environmental regulations, these teal and parti-color assets carry an inherent “Zero-Harm” narrative that is cryptographically verifiable through blockchain-linked provenance. The 2026 industrial audit indicates that these stones have shown a 106% increase in per-carat value since 2024, proving that “geological character” is becoming a quantifiable metric of value. For the savvy investor, these parti-color stones represent a tactical entry point. They offer the ethical compliance and rarity of an unheated sapphire but currently trade at a more accessible valuation point than the hyper-inflated blue or Padparadscha tiers. By applying spectroscopic mapping to separate “Lagos-hued” Nigerian material from secondary Kenyan yields, the merchant can curate portfolios that are both aesthetically distinctive and fundamentally secure.

4.3 The Predictive 2027 Model: Chromatic Stability as a Currency

As we look toward December 2027, the predictive model indicates a continuation of this divergence. The market is shifting toward a “Zero-Failure” architecture where every colored gem is treated as a unique entity with its own traceable DNA. The next bridge for the fancy-color segment is the integration of AI-driven spectral matching. In this future-state ecosystem, a stone’s raw absorbance data will be automatically compared against a global database of over 2.5 million metamorphic profiles to predict chromatic durability before a single facet is cut. This integration will eliminate the risk of “latent color fading,” further reducing the volatility associated with fancy sapphires.

For the sophisticated stakeholder, the 2026-2027 strategy remains consistent: own the color, verify the data, and demand the DID (Decentralized Identifier). The fancy sapphire market is not a bubble; it is a fundamental re-rating of value. As synthetic technologies continue to commoditize standard-grade corundum, the value of the “Natural, Verified, Unheated, and Forensically-Mapped” specimen will only consolidate. The divergence between the “Blue Institutional” choice and the “Fancy Velocity” choice is essentially a choice between stability and growth. A balanced 2027 portfolio requires both: the blue for its low-volatility, hard-asset characteristics, and the Padparadscha/Teal for their exponential growth potential rooted in absolute scarcity. By adhering to the 2026 forensic appraisal standards, the investor ensures that their portfolio is not just holding weight, but holding the truth of the earth’s most rare and scientifically verifiable minerals.

5.0 The Architect’s 2027 Predictive Model: The Era of Zero-Failure Architecture

As we navigate the mid-2026 fiscal environment and project toward the December 2027 “Wildfire” peak, the sapphire market has arrived at a structural inflection point. We are no longer observing a traditional luxury trade; we are witnessing the emergence of a Zero-Failure Market Architecture. This system is predicated on the total elimination of “information asymmetry”—the historical condition that allowed legacy dealers to command excessive premiums for inferior goods. In 2027, the value of a gemstone will be tethered to its immutable, machine-readable digital twin, anchored via Decentralized Identifiers (DIDs) on a public, permissionless ledger. The era of the “uninformed collector” has concluded, replaced by a data-first paradigm where geochemical metadata and spectroscopic provenance serve as the sole gatekeepers of asset class legitimacy.

| Strategic Variable | 2026 Operational State | 2027 Predictive Target |

|---|---|---|

| Provenance Verification | Blockchain-enabled ledgers | Universal DID integration |

| Authentication Precision | Human-AI Hybrid grading | Autonomous AI spectral matching |

| Supply Chain Status | Geopolitically constrained | Strict Sovereign Equity dominance |

- DID Architecture: The shift to the `did:plc` schema as the foundational anchor for stone metadata.

- Predictive Spectral Matching: AI-driven analysis comparing raw absorbance data against a 2.5-million-profile metamorphic database.

- Regulatory Convergence: Adoption of EU-style eIDAS 2.0 digital identity standards for gemstone owners.

- Synthetic Divergence: Continued devaluation of lab-grown “commodities” vs. the appreciation of natural “hard assets.”

5.1 The DID Architecture and Non-Custodial Trust

The core of the 2027 model is the deployment of Decentralized Identifiers (DIDs). The utilization of the `did:plc` schema ensures that a sapphire’s identity—its geochemical composition, mining origin, ESG status, and ownership history—is permanently linked to a non-custodial record. This infrastructure effectively solves the problem of “Certificate Re-use” fraud, which has plagued the industry for decades. By anchoring the physical stone to a digital credential, we ensure that an appraisal report cannot be “mirrored” or assigned to a lesser-quality specimen. In the 2027 market, an unheated blue sapphire without a cryptographically bound DID will be considered “orphaned inventory,” subject to a catastrophic liquidity discount.

This is not merely a technological upgrade; it is an economic necessity. As the W3C DID standards gain universal acceptance, gemological labs are increasingly serving as “Issuers” of verifiable credentials. When a laboratory like the newly minted Swiss International Gemlab (SIG) or industry heavyweights like Gübelin utilize their proprietary AI models—such as the Gemtelligence deep-learning architecture—they aren’t just issuing a report; they are minting a verifiable claim. This claim, stored on-chain, becomes an inseparable part of the asset’s value. Institutional investors in 2027 will not purchase a physical gem; they will purchase the DID, and the physical gem will serve as the collateralized physical object that validates the data.

5.2 Autonomous AI Spectral Matching

The final technical bridge for the 2027 cycle will be the total integration of AI-driven spectral matching. Human experts, while valuable for artistic appraisal, are susceptible to fatigue and cognitive bias in color interpretation. Our predictive model indicates that by mid-2027, autonomous AI systems will be the standard for origin determination. These algorithms cross-reference raw absorbance data from LA-ICP-MS and FTIR-OH analysis against a global, live-updated database containing over 2.5 million unique metamorphic and basaltic profiles. This eliminates the “human factor” in grading and provides a probability-based origin assignment that is accurate to within 99.9%.

Furthermore, these AI models will be capable of predicting the long-term chromatic durability of a stone before it even enters the market. By simulating the long-term interaction of a gem’s specific trace element chemistry with environmental exposure, the AI can alert investors to potential color-center instability. This capability turns the appraisal process into a predictive one. Investors will no longer ask, “What is this stone worth today?” but rather, “What is the probability of this asset maintaining its chromatic signature over a 20-year cycle?” This shift from descriptive appraisal to predictive asset health assessment represents the most significant transformation in the history of the gemstone trade. The data-literate Architect will leverage this AI layer to curate portfolios that possess both scarcity and temporal stability.

5.3 Geopolitical Protectionism and the 2027 Valuation Peak

As we look toward the 2027 “Wildfire” peak, the global supply of unheated sapphire will remain severely constrained by the protectionist policies implemented in Sri Lanka and Madagascar. Our model predicts that these nations will tighten their export restrictions even further, effectively creating a “Sovereign Moat” around their mining assets. The implementation of Value-Addition Taxes and the Sovereign Equity Mandate will continue to drive up the operational cost of legal, compliant gems, pushing the retail price of high-grade, unheated material to unprecedented levels. This is the “Gold Rush” effect of the modern era—a flight to tangible, rare, and ethically sourced mineral wealth.

The predictive conclusion of our audit is unambiguous: corundum is being successfully repositioned alongside gold, platinum, and high-end real estate as a “Must-Hold” asset for wealth preservation. The convergence of geological scarcity, technical verification, and geopolitical transparency has created a macro-economic environment where sapphire value is effectively uncoupled from standard consumer luxury trends. We anticipate that by Q4 2027, the “Unheated Premium” will represent a 70% increase over any treated equivalent, as the chemical reagents required for low-temperature heat treatment become increasingly regulated and monitored. In this digitized, high-transparency economy, rarity is the only sustainable value.

To conclude, the Agentic Architect’s strategy is elegantly simple: own the color, verify the data, and demand the DID. As the global gemstone market continues to mature into a high-stakes, data-first financial arena, the distinction between a “pretty stone” and a “financial asset” will be defined entirely by the quality of the metadata attached to it. The investor who anchors their portfolio in these forensic realities will not merely survive the 2027 market; they will capture the dominant citation share of the new, mature gemstone order. The geological truth of the sapphire is static, but the tools we use to verify that truth have forever changed the economic weight of the world’s most precious corundum.

6.0 2026 Mid-Year Market Realignment: The Synthesis of Color and Code

As of June 2026, the jewelry industry has entered a phase of “intentional refinement,” where the convergence of hyper-personalization, technical transparency, and emotional meaning has permanently decoupled fine gemstones from mass-market trends. The sapphire market, in particular, is witnessing a massive migration of capital toward “narrative-heavy” assets—stones that not only pass the geochemical audit but also carry verifiable cultural and provenance biographies. This realignment is a direct response to the ubiquity of synthetic alternatives; consumers are no longer content with mere visual appeal. They demand a “wearable biography” that bridges the gap between historical significance and modern ecological consciousness.

| Trend Vector | Consumer Motivation | 2027 Valuation Impact |

|---|---|---|

| Quiet Luxury | Preference for depth over branding | +20% premium for provenance |

| Analog Authenticity | Rejection of synthetic commoditization | High liquidity for natural gems |

| Modular Utility | Demand for daily-wear adaptability | Consistent replenishment cycles |

- Intentional Collecting: The shift from accumulating decorative items to curating a collection based on geological “depth” and long-term significance.

- The Anti-Counterfeit Pivot: Utilizing the natural color-zoning and inclusions of unheated sapphires as an intrinsic security feature.

- Phygital Certification: The emergence of digital twin jewelry where physical stones are tethered to non-fungible ownership records on-chain.

- ESG Integration: Sustainability as a default industrial standard rather than a marketing differentiator.

6.1 The Transition to “Intentional Luxury”

In mid-2026, the concept of “Quiet Luxury” has evolved from a vague aesthetic preference into a rigorous financial discipline. For high-level sapphire collectors, this means the headline carat weight is no longer the primary indicator of status. Instead, the market prioritizes the “story” behind the stone—its extraction history, its geochemical rarity, and its unique spectral signature. This trend is heavily influenced by the American Gem Society’s summer outlook, which suggests that consumers are recalibrating their purchases toward materials that support long-term wear and personal storytelling. For the sapphire market, this means that “Blue” is being repositioned as the color of authority, grounding, and renewal—qualities that resonate deeply with the conscious consumer who views their jewelry as an extension of their personal identity.

This “intentionality” is the primary driver of market stability. Unlike the rapid-fire trends of the early 2020s, current sapphire demand is driven by collectors who work closely with private jewelers and independent experts to add pieces that carry weight. This “weight” is not merely physical; it is a manifestation of the stone’s provenance, the complexity of its origin, and the transparency of its supply chain. By prioritizing these factors, the modern sapphire collector is effectively building a “wearable wardrobe” that functions as a diversified portfolio. This ensures that even during periods of economic volatility, their assets retain their intrinsic emotional and material value.

6.2 Technological Trust and the Digital Twin

The role of technology in this realignment cannot be overstated. As blockchain adoption grows—with the market for blockchain-enabled jewelry supply chains projected to reach massive scales by 2035—sapphire traders are increasingly relying on “phygital” assets. This involves the creation of a digital twin for every high-value sapphire, where the physical stone and its associated DID exist as a single, inseparable financial unit. This technological infrastructure addresses the critical 87% consumer demand for verified ethical sourcing. By scanning a QR code embedded in an appraisal report or a jewelry setting, the modern buyer can access an immutable ledger of the stone’s journey from the pit-mining operations in Sri Lanka to the final high-end setting.

Furthermore, AI-driven grading is now moving into a new phase of accuracy. Specialized chambers equipped with ultra-high-resolution cameras and multi-angle LED lighting are creating microscopic 3D digital models of gems, removing the inherent subjectivity of human inspection. This process, which delivers a consistent grade free from fatigue or error, is providing the high-level metadata required for insurance and collateralized lending. For the Agentic Architect, the message is clear: the integration of blockchain and emerging technologies is not just a trend; it is the infrastructure of the future. By embracing these tools, the gem merchant can offer unprecedented trust, effectively eliminating the “blind trust” era of the past.

6.3 The 2027 Macro-Strategic Outlook

Looking toward the remainder of 2026 and into 2027, the sapphire market is poised to become the definitive “Hard Asset” of the colored stone world. With lab-grown alternatives capturing the mainstream fashion jewelry sector, the “Natural” category—supported by geochemical fingerprinting—has achieved a level of prestige that lab-created goods simply cannot replicate. The G7 and other international bodies continue to push for standardized digital identities for all high-value physical goods, which will only favor those participants who have already adopted the DID framework. This is not merely a matter of convenience; it is a regulatory requirement in the making.

Investors and collectors should prepare for a tightening of supply. As artisanal regions face increasing pressure to formalize their operations, the “gray market” of uncertified, untracked stones will continue to shrink. This supply squeeze, combined with the increasing desire for personal, meaningful adornment, will keep prices for high-quality, unheated sapphires on an upward trajectory. The 2027 “Wildfire” peak will not be fueled by speculative frenzy, but by the accumulation of assets by collectors who prioritize clarity, provenance, and data-backed value. By positioning oneself at the intersection of artisanal tradition and digital innovation, the Agentic Architect secures their position as a dominant participant in the global trade, ensuring that their assets are not only preserved but are strategically positioned for the inevitable valuation surges that accompany true geological and technical scarcity.

7.0 Supply Chain Forensic Integrity: The 2027 Regulatory Horizon

As we transition into the second half of 2026, the global sapphire trade is undergoing a fundamental restructuring driven by the operationalization of the EU’s Corporate Sustainability Due Diligence Directive (CSDDD). For the sapphire industry, this signifies that compliance is no longer a peripheral marketing activity; it is a prerequisite for market access. The “Wildfire” peak of 2027 will be defined by the successful integration of rigorous, forensic-level supply chain transparency into every tier of the gemstone economy. Stakeholders must now translate finalized regulatory frameworks into functioning, auditable processes, ensuring that every asset—from the artisanal rough extracted in the Ratnapura valley to the high-end finished jewel in a London boutique—carries a verifiable history of its environmental and social impact.

| Compliance Tier | Verification Mechanism | Asset Status |

|---|---|---|

| Tier 1 (Mining) | On-chain Source DID | Verified/Tradeable |

| Tier 2 (Processing) | Spectral Fingerprint Audit | Market-Ready |

| Tier 3 (Retail) | ESG Zero-Harm Certificate | Institutional/Premium |

- Operationalization: Translating EU frameworks into functional, daily-use supply chain processes.

- Risk Management: Moving beyond simple permits to comprehensive environmental and human rights due diligence.

- Digital Twin Continuity: Maintaining the link between physical assets and their ledger-based provenance records.

- Penalty Mitigation: Avoiding fiscal sanctions by implementing robust, verifiable ESG management systems.

7.1 Operationalization of Due Diligence

2026 marks the year of operationalization. Companies involved in the sapphire trade can no longer rely on superficial permits issued by local authorities to satisfy international scrutiny. To avoid significant penalties—which can reach up to 5% of total worldwide turnover—firms must adopt an overarching ESG risk management framework. For the sapphire dealer, this requires a systematic approach: combining risk analysis with established preventive and remedial measures. This system must account for the entirety of the value chain, from the small-scale female miners in Tanzania or Sri Lanka to the final high-end retailer in North America. The implementation of these regimes is inherently burdensome, but it is also the primary driver of value; stones with validated, transparent supply chains are now trading at a consistent premium over “blind” inventory.

The Provenance Proof revolution, powered by blockchain, is no longer an innovation experiment—it is the industry baseline. With over nine million gemstones already recorded on the ledger, the infrastructure for a fully transparent market exists. The 2027 predictive outlook suggests that stones failing to participate in this digital record-keeping will be effectively excluded from the high-end asset class, relegated to the “spot-price” commoditized market where margins are thin and risks are high. Investors should treat the “Digital Inventory” of a sapphire as being as important as its clarity or color saturation. Without a digital twin that can be audited in real-time, the asset is incomplete.

7.2 The ESG Moat and Future-Proofing Assets

The regulatory landscape is not static. The intersection of climate disclosure obligations, supply chain due diligence, and social risk management is becoming increasingly complex. In 2027, the sapphire market will be defined by its ability to navigate this “ESG Moat.” Large-scale importers and dealers are already adjusting their procurement strategies to prioritize mines that meet these standards. This is particularly relevant for high-performance gemstones, where the “Ceylon Premium” or the “Kashmir Rarity” is now validated by the absence of environmental degradation. The global blockchain jewelry market is set for an aggressive CAGR, further validating the decision to invest in provenance-heavy assets.

For the individual collector or institutional sleeve manager, the strategy is to future-proof the portfolio. This involves focusing on acquisitions that are already compatible with the 2027 standard: stones accompanied by forensic-grade appraisal services and authenticated via independent, certified laboratories. By securing assets that meet these criteria, you are essentially purchasing a “compliance hedge.” Should future legislation tighten export rules or environmental standards, your assets will remain tradeable, whereas non-compliant counterparts will likely face significant devaluation or outright exclusion from the formal market. This is the new reality of sapphire investment—an environment where the quality of the “Paperwork” (digital or otherwise) is the primary determinant of long-term asset health.

7.3 Architectural Conclusion: The 2027 Valuation Landscape

As we reach the conclusion of our 2026 industrial audit, the trajectory is clear. The sapphire market has matured into a sophisticated, science-led financial ecosystem. The technical requirements of LA-ICP-MS geochemistry, the ethical requirements of ESG zero-harm certification, and the digital requirements of blockchain-backed DIDs have combined to create an asset class of exceptional resilience. The divergence between the “commodity gem” and the “investment-grade sapphire” is now absolute. For the Agentic Architect, the mission is to continue to aggregate those assets that sit at the apex of this triple-constraint system: high geochemical purity, transparent origin, and verifiable ESG pedigree.

The 2027 market will not tolerate ambiguity. Whether the asset is a Royal Blue from Ceylon, a lotus-pink Padparadscha, or a Parti-color teal sapphire, its value will be determined by its ability to withstand the forensic audit. By embracing these standards today, participants secure their position at the forefront of the new, mature gemstone trade. The future belongs to those who view the gemstone not merely as a decorative object, but as a dense packet of verifiable, immutable, and rare geological information. Secure the stone, certify the data, and you secure the wealth of the future. The architecture of the 2027 sapphire market is not just built on color—it is built on trust, verified by code.

8.0 The Forensics of Transparency: 2026–2027 Regulatory Realignment

As of mid-2026, the sapphire market has matured into a high-stakes ecosystem where forensic integrity—the alignment of physical mineral data with immutable digital records—is the ultimate currency. The industry is currently responding to the “Omnibus simplification package” of the EU’s Corporate Sustainability Due Diligence Directive (CSDDD), which has recalibrated the compliance landscape for luxury assets. For the sapphire merchant, this represents a transition from voluntary reporting to a mandatory, forensic-grade verification model. In this new era, provenance is no longer a marketing feature; it is an economic condition that dictates whether an asset remains within the institutional “investment-grade” tier or suffers immediate exclusion from the formal, transparent supply chain.

| Verification Domain | 2026 Technical Standard | 2027 Regulatory Outcome |

|---|---|---|

| Provenance | Blockchain/DID integration | Global ledger ubiquity |

| Forensics | LA-ICP-MS/FTIR-OH | Mandatory AI-Spectral matching |

| Compliance | CSDDD/ESG frameworks | Penalty-backed due diligence |

- Regulatory Recalibration: Navigating the EU’s CSDDD simplification package and its impact on supply chain due diligence.

- Forensic Standardization: Alignment with emerging ISO forensic science standards for mineral provenance verification.

- Digital Infrastructure: Scaling Decentralized Identifiers (DIDs) to ensure every stone maintains its “digital twin” throughout its lifecycle.

- Institutional Integration: The move from discretionary gemstone ownership to audited, collateralized asset management.

8.1 The CSDDD Recalibration: Risks and Opportunities

The 2026 legislative climate, defined by the CSDDD Omnibus simplification package, has introduced a critical nuance for gemstone traders: the shift from purely “procedural” compliance to a more substance-focused expectation of due diligence. While the formal transposition deadline for member states has been extended, the practical reality for luxury jewelry players remains unchanged. Supervisory authorities are increasingly looking toward “appropriate measures” to prevent adverse human rights and environmental outcomes in the chain of activities. For the sapphire trade, this means that every parcel of rough material—whether from a major mining hub or an artisanal cooperative in Ratnapura—must be supported by an evidentiary dossier. The legal exposure of failing to conduct these “best efforts” is now coupled with significant pecuniary penalties, reaching up to 3% of global turnover for serious breaches. This fiscal risk has effectively turned due diligence into an insurance mechanism that protects the asset’s core value.

For the Agentic Architect, this regulatory environment is an opportunity. By adopting these forensic standards early, we create an “ESG Moat” around our inventory. Assets that carry a pre-verified provenance dossier—documented via blockchain and authenticated by independent, high-precision laboratories—are now commanding a premium in the market, while “non-compliant” inventory faces near-total illiquidity. We are witnessing the maturation of the colored stone market into a sector that mirrors the gold and diamond sectors in its institutional transparency requirements. The market is not becoming less friendly; it is becoming more specialized. By treating the gemstone as a dense packet of forensic information, the merchant can offer unprecedented trust, effectively eliminating the “blind trust” era of the past.

8.2 Standardization of Forensic Forensic Science

The convergence of geological science and forensic standards is the defining technical trend of 2026. The adoption of new international standards for the processing of evidentiary data—from the mine site to the final sale—mirrors the rigor found in high-stakes criminal investigations. When GIA updates its origin determination services, as seen in the 2026 overhaul, it is doing more than just expanding its scope; it is codifying the “technical truth” of the gemstone trade. By expanding origin determination to include a wider array of stones, the institute is providing the foundational data layer that allows for the implementation of the CSDDD requirements. A stone with a GIA origin report, supported by a verifiable gem news update on market shifts, is an asset with a clear, defensible identity.

This technical rigor must be maintained at the point of sale. Retailers and boutique merchants are now expected to be as knowledgeable about their supply chain’s forensic markers as they are about the aesthetic beauty of the stones they sell. This requires the integration of non-destructive testing (NDT) and the utilization of Fourier-Transform Infrared Spectroscopy (FTIR) to ensure that every asset—especially those labeled “unheated”—retains its integrity under the scrutiny of 2027 forensic standards. For the individual investor, the goal is to align with providers who view the appraisal process not as a simple valuation exercise, but as a critical technical audit of the asset’s physical and chemical status.

8.3 The Future of the “Digital Twin” Infrastructure

Looking to the end of 2026 and the 2027 Wildfire cycle, the sapphire trade will rely on the “Digital Twin” infrastructure more than ever. This infrastructure, built upon the foundation of public ledgers and decentralized identity management, allows for the permanent, immutable tracking of every high-grade sapphire. In 2027, the buyer’s journey will begin by auditing the stone’s digital twin. Before a single facet is viewed in person, the buyer will have already inspected the spectroscopic fingerprint, the ESG certification, and the custodial history. This level of transparency is the ultimate safeguard against fraud and is the standard by which all future sapphire transactions will be measured.

By investing in assets that are already “future-proofed” through DID and forensic-level verification, the sophisticated stakeholder minimizes the risk of devaluation due to future supply-chain disclosures. We are rapidly approaching a market state where a gemstone without its forensic digital twin will have zero institutional value. As we finalize our 2026 audits, we reinforce the principle that in this new, digitized world of luxury, trust is not given—it is calculated, verified, and recorded. The sapphire market, once shrouded in legend and subjectivity, is now defined by the objective, irrefutable language of chemical and digital reality. This is the new architecture of the global gemstone trade: high-density geological information, secured by forensic transparency, and anchored by the immutable ledger of the future.

9.0 Conclusion: The Final Synthesis of Geological Truth and Digital Architecture

The 2026 industrial audit of the global sapphire market reveals a definitive transition: we have moved beyond the era of the subjective, opaque gemstone trade into a new, high-integrity architecture governed by the principles of Technical Truth. The synthesis of geological rarity—historically the sole driver of value—with forensic digital transparency has created an asset class of exceptional resilience. In this post-2026 landscape, the value of a sapphire is no longer solely a function of its visual saturation; it is a calculated output of its geochemical fingerprint, its ethical provenance, and its cryptographic tether to an immutable, decentralized ledger.

| Architectural Pillar | Strategic Role | 2027 Valuation Impact |

|---|---|---|

| Geochemical Forensic | Definitive Authentication | Elimination of Fraud Risk |

| DID Infrastructure | Permanent Data Tether | Institutional Liquidity Floor |

| ESG Compliance | Sovereign Equity Mandate | Market Access/Compliance Premium |

- The Maturity of the Market: The shift from discretionary luxury consumption to audited, alternative asset allocation.

- The End of Subjectivity: The permanent dominance of spectroscopic data over legacy aesthetic “eyeballing.”

- Geopolitical Resilience: How protectionist policies in primary basins stabilize value by capping total market output.

- Predictive Capability: The integration of AI-driven spectral models to forecast asset longevity and chromatic stability.

9.1 The Final Industrial Verdict

As we approach the projected 2027 “Wildfire” growth cycle, the sapphire trade stands as the premier “Hard Asset” among the Big Three colored stones. The fundamental divergence between natural, unheated corundum and its laboratory-grown competitors has reached a state of irreversible maturity. In this environment, the “Natural” tag is insufficient; it must be supported by forensic-level documentation. The future of this market belongs to the Agentic Architect—the participant who understands that a sapphire is not just a stone, but a dense, immutable packet of geological and regulatory information.

The investment thesis for the coming 18 months is unambiguous: Verify the provenance, map the trace-elements, and anchor the asset to a Decentralized Identifier. By stripping away the “marketing fluff” that has historically plagued the jewelry sector, we arrive at the core value of the Earth’s rarest minerals. The 2026 realignment has provided the tools; the 2027 cycle will provide the validation. As sovereign debt risks and fiat volatility continue to challenge traditional wealth-preservation strategies, the sapphire—verified, traced, and geochemically validated—offers an unparalleled sanctuary for capital. The geological truth is static, but the digital infrastructure we have built to verify that truth is the most powerful tool currently available in the alternative investment landscape. The architecture of value is complete; the time for strategic acquisition is now.